This page is for Tax Attorneys, CPAs, CFOs and other Tax Experts

The structure of the CP+PLUS Plan has been available since 1954 and has been backed by an IRS Revenue Ruling since 2012. If you are interested in understanding the legitimacy of the program, you may read further by downloading the CP+PLUS WHITE PAPER 2018 as well as the reviewing the endorsements and articles below.

If you have any questions at all, please reach out directly to Roger Jeffrey, our CEO.

Click Here to Read the

CP+PLUS WHITE PAPER 2018

Simple: The Plan Structure Has Been

Allowed Since 1954!

I.R.C. Sections 61 and 62 have been in the tax code since 1954. These sections make it clear that an employee and their employee can establish an arrangement where the employee can allocate the portion of their wages they use for un-reimbursed business expenses and have their employer convert the money into a tax-free business expense reimbursement plan.

CP+PLUS Automated System Means Little Work for the Employer!

The CP+PLUS Business Expense Reimbursement System can indeed streamline processes and reduce the workload for employers. Here are some ways it can help:

- Automation: CP+PLUS automates many aspects of expense reporting, such as receipt capture, expense categorization, and policy compliance checks. This eliminates the manual effort required from both employees and finance teams.

- Integration: It integrates with various accounting and payroll systems, ensuring seamless data transfer and eliminating the need for manual data entry.

- Policy Enforcement: CP+PLUS can automatically enforce company policies, flagging non-compliant expenses and eliminating the need for manual reviews.

- Reporting and Analytics: It provides detailed reporting and analytics, helping employers prepare for audits. Saves valuable time and efficiency.

- Mobile Access: Employees can submit expenses on the go using mobile devices, which can speed up the reimbursement process, keeps them in tax compliance, reduces time and the storage of their business receipts.

Overall, while there may be an initial setup and training period for the employees, the long-term benefits of using the CP+PLUS system lowers payroll taxes for both employee and employer, while eliminating almost all the workload in a typical business expense reimbursement plan for the employer.

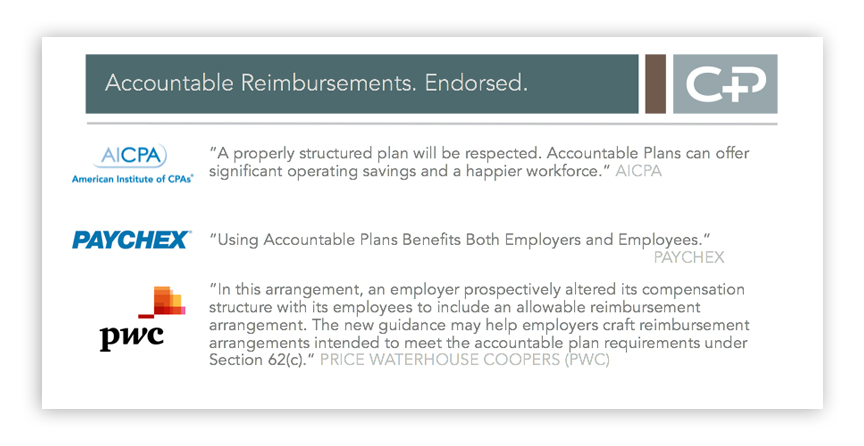

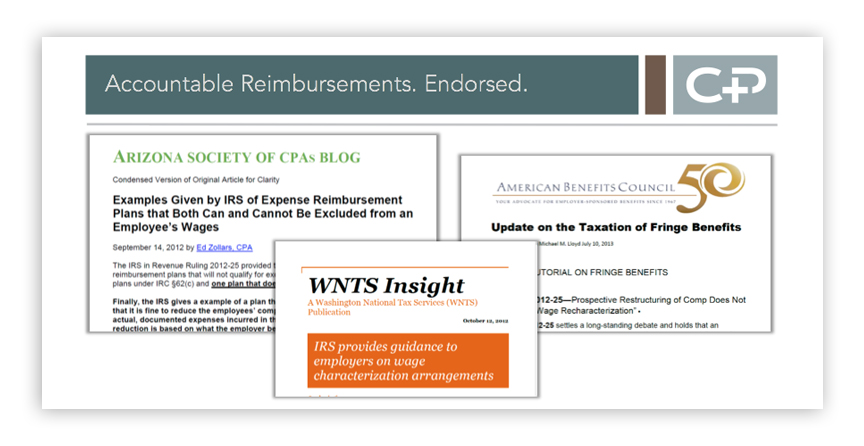

Articles and Endorsements from other Tax Experts

Can you Deduct Unreimbursed Job Expenses?

Click Title to Go to Article

Written by Dr. Stephen Fishman

"The Tax Cuts and Jobs Act completely eliminated all miscellaneous itemized deductions subject to the 2% of AGI limit, including the deduction for unreimbursed employee expenses. Thus, employees who spend their own money for things like job related car expenses, travel, education, or tools get no deduction at all. The deduction for unreimbursed employee expenses is scheduled to return in 2026. . . . This makes it more important than ever to seek reimbursement for such expenses from the employer."

Tax Surprises: Check Out this List of Individual Tax Deductions that are Just Gone

Download PDF:

Tax Surprises .Philly News

Written by Erin Arvelund

"Unreimbursed employee business expenses: For a lot of people, this will be a game changer. Employers may be able to help employees in reversing the lost tax benefit.". . . "with the new law, it’s taken on heightened significance.” “If you’re an employee paying for business meals, vehicle, travel, entertainment of clients, those won’t be deductible by employees anymore,” . . . "Employers can set up what’s known as an “accountable plan” with rules about what’s reimbursable and what’s not. Union dues, for instance, are an employee expense that’s no longer deductible" . . . “Everyone has to re-evaluate how much they withold from their paychecks, especially if they were heavy users of itemized deductions before the new law.”

Tax Reform Suspends the Tax Deduction for Employee Business Expenses

Download PDF:

ACTAX Article

Not all provisions of the Tax Cuts and Jobs Act are beneficial to taxpayers. One notable negative provision is the suspension of the deduction for employee business expenses. Under prior law, taxpayers who were employees were able to deduct expenses related to their employment as a miscellaneous itemized deduction, to the extent the expenses exceeded 2% of their adjusted gross income. Yet, under the tax reform, employee business expenses will not be allowed for tax years 2018 through 2025." . . ."The only possible remedy for the loss of this deduction is for an employee to negotiate an “accountable plan” with the employer."